Understanding the Annual EBF Spending Plan Requirement

By Luke Corry

Beginning with the fiscal year 2024 budget cycle, school board members will find a new tab within the annual district budget form — the Evidence-Based Funding (EBF) Spending Plan. District leaders have submitted EBF Spending Plans since the enactment of the 2017 Evidence-Based Funding for Student Success Act (105 ILCS 5/18-8.15). This legislation overhauled the state funding formula and included a new requirement to describe the intended use of state dollars. Specifically, the statute provided that all organizational units, defined as those entities that are eligible to receive Tier Funding, submit a plan that describes 1) how they will achieve student growth and make progress toward state education goals, 2) the intended use EBF dollars, and 3) the intended use of dollars within the funding formula that are specifically attributable to special education costs and students who are low-income or English learners (ELs).

School board members and district leaders now have a new opportunity to engage in discussion about the intended use of state funding. To date, spending plans have been completed and submitted in the ISBE Web Application Security (IWAS) system, which is only accessible to district administrators; ISBE has not published spending plan responses. Incorporating the spending plan into the budget template means that spending plan responses will be public starting with FY 2024. The information in this text is intended to support school board members in understanding the spending plan content and how it can contribute to productive local dialogue about resource allocation.

Aligning the Spending Plan Requirement with a Value Proposition

Aligning the Spending Plan Requirement with a Value Proposition

The ISBE 2020-2023 Strategic Plan included three primary goal areas: Student Learning, Learning Conditions, and Elevating Educators. The Learning Conditions goal area specifically addressed the need to support districts in strategic resource allocation decision-making. One aligned initiative included revising the spending plan requirement with a goal to identify how it could support local decision-making about the equitable allocation of resources. ISBE convened an advisory group in the fall of 2021 to evaluate possible revisions. The group consisted of a broad cross-section of superintendents, program and finance leaders within organizational units, and advocacy groups.

Before considering revisions to the spending plan, the group staked out three objectives — to establish a value proposition to guide the work, to identify a new location for the spending plan within an existing report that would add the most value, and to align the content of the spending plan with the value proposition.

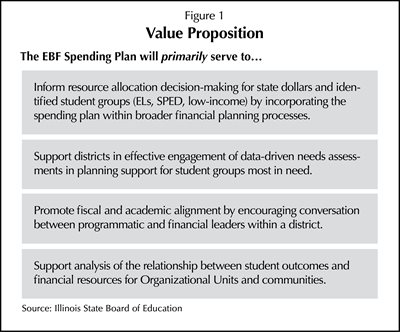

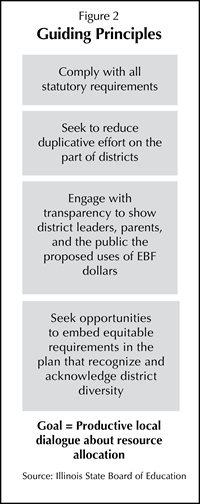

The group next turned its attention to crafting a value proposition and articulating principles that would guide the work. They quickly landed on the goal of supporting productive local dialogue about resource allocation. Along the way, the group committed to looking for opportunities to simplify the content and increase transparency regarding the use of EBF (See Figure 1).

The advisory group considered several options for placing the plan within another required report. Ultimately, state statute provided a source of inspiration: Illinois School Code specifies that a spending plan should be completed as part of the budget process. Including a spending plan in the annual budget form that districts transmit to ISBE aligns in several important ways with the value proposition and guiding principles (Figure 2). Specifically:

- Inclusion allows for the consolidation of two pla

nning requirements. Planning for the spending plan can now occur within the scope of activities included in the budget process.

nning requirements. Planning for the spending plan can now occur within the scope of activities included in the budget process. - Districts must hold a public hearing prior to adopting a budget, and final budgets must be published on district websites (per statute). Spending plan responses can now be a part of these procedures for ensuring trans-parency in financial decision-making.

- Districts are best positioned to maximize resources when they consider them together. The budget process culminates in a plan for all revenues. The spending plan encourages planning for state dollars alongside all revenue streams.

Understanding the Plan Content

Incorporation into the budget template means the spending plan now has two audiences — the district staff who will complete it and the stakeholders, including school staff, board members, and parents, who will read it. Members of the advisory group kept these two audiences in mind as they considered revisions to the plan content. In terms of structure, the plan largely follows the template of prior spending plans; it will certainly be familiar to staff who have completed it in the past. Some questions are the same, and many items continue to be answered by selecting responses from a provided list. As with previous spending plan templates, users can indicate an “other” response and provide additional context.

With the second audience — stakeholders — in mind, the spending plan questions are designed to be under-standable without financial expertise. Of course, state funding formulas can be complicated, and EBF is no exception. The ISBE EBF Spending Plan webpage will include definitions for key terms to support communities in understanding spending plan responses. Below, we highlight a few important terms to know. School board members with questions about the mechanics of the formula are encouraged to review the spending plan webpage as well as previously pub-lished materials. Additional resources are available at the resources link below.

- Adequacy Target: EBF provides an estimated minimum cost of educating students in each district. The formula accounts for actual local enrollment to calculate adequate spending. As an educational concept, adequacy refers to providing a sufficient level of resources to meet learning standards. Importantly, the Adequacy Target is not actual funding; it is simply an estimate of adequate resources for each district.

- Cost Factors: To calculate the Adequacy Target, EBF applies statute-defined staffing ratios, as well as per-student amounts for other common expenditures, to district enrollment. Some cost factors account for staffing expenditures, while others, like professional development and technology, estimate costs on a per-student basis. The Adequacy Target includes additional investments to account for the cost of providing more support for students who require special education services or who are English learners or low-income.

- Base Funding Minimum: The Base Funding Minimum (BFM) is a hold-harmless provision that ensured each organizational unit would receive an amount at least equal to what it received in FY 2017 from five grant programs: General State Aid, Special Education – Personnel, Special Education – Funding for Children Requiring Special Education Services, Special Education – Summer School, and English Learner Education. Each year that districts receive Tier Funding, that funding becomes part of the next fiscal year’s BFM, so districts are always receiving at least the funding that they received the year prior. The BFM will also include prior year Property Tax Relief Grant amounts if distributed the prior year and received by an Organizational Unit.

- Final Resources: The EBF formula considers the local capacity of each district to fund education. This calculation uses the Local Capacity Target (a measure of local wealth), the Base Funding Minimum, and Corporate Personal Property Replacement Tax revenue to determine available resources.

- Percentage of Adequacy: Each district’s Percentage of Adequacy is calculated by dividing its Final Re-sources by the Adequacy Target to determine how far each district is from having the minimum resources it needs. The resulting percentage determines a district’s Tier Assignment, which drives the distribution of Tier Funding.

- Tier Funding: Appropriations for EBF above the Base Funding Minimum amount are available for dis-tribution as Tier Funding. Districts are eligible to receive Tier Funding based on their Tier Assignment. Districts in Tiers 1 and 2 have the lowest Percentages of Adequacy. EBF directs 99% of Tier Funding to these districts. The remainder is distributed to districts in Tiers 3 and 4, which have Percentages of Adequacy equal to or greater than 90%.

Some portion of Tier Funding may be attributable to ELs, low-income students, or students who require special education services. ISBE calculates this percentage annually.

A Window into the Use of State Funds

The incorporation of the EBF Spending Plan into the public budgeting process provides new opportunities for local communities to discuss resource allocation. District leaders can leverage the spending plan to show how the use of state dollars is connected to important goals and strategies for improvement. Community members can ascertain how districts are engaging with timely data and local stakeholders to inform their decisions. Specifically, the spending plan will provide:

- A statement of goals for student success and three strategies for pursuing those goals.

- Available resources from state funding, including current year Tier Funding and the total amounts at-tributable to students who are English learners, low-income, or who require special education services.

- Detail regarding how Tier Funds will be spent.

- A list of the stakeholders who were consulted and the data that was reviewed to determine spending.

- Additional detail regarding the intended use of funds for specific student groups and a set of assurances regarding the consultation and spending requirements for ELs (105 ILCS 5/14C).

The spending plan provides new information for local communities but has certain limitations. The School Code includes requirements for the use of funds attributable to specific student groups, but EBF is otherwise a flexible revenue source for districts. As with local dollars, districts have broad discretion over the use of state funds.

The spending plan uses the EBF Cost Factors as a framework for districts to indicate planned investments. However, each district’s spending needs are unique to its students and community context, and there is no requirement that districts allocate their funds according to the Cost Factors. Additionally, certain questions allow districts to enter a dollar amount for budgeted expenditures.

However, the state chart of accounts does not require that districts separately account for expenditures from state funds. Any budgeted expenditure figures included in the spending plan are best interpreted as approximations of spending and not figures that can be directly tied back to other financial reports. Finally, state resources make up just one source of district revenues. The EBF Spending Plan is primarily focused on the intended use of state funding, but districts coordinate local, state, and federal funds to build programs. This context is important to consider when reviewing spending plan responses.

School Boards and the EBF Spending Plan

The Illinois School Code established budget requirements, including the development of a tentative budget, public hearings, and final adoption, for districts. School boards have a formal role in these processes and are ultimately responsible for approving a budget. The School Code does not specifically require school boards to approve EBF Spending Plans, but the plan’s inclusion in the budget form is intended to increase collaboration and discussion. School boards and local communities can ask and answer critical questions about local use of EBF, such as:

- How do the spending decisions represented here reflect the district’s strategic priorities?

- Who was engaged in the decision-making process? What data was considered?

- If eligible for Tier Funding, how are Tier Funds addressing student needs?

- What state funds are available to support high-need students? How are they being used?

- How are state resources combined with other available local and federal funds to support all students?

Districts are encouraged to include the spending plan in the tentative budget and public hearings. In this way, board members and all stakeholders have a new chance to engage in dialogue about the use of state resources. This article has provided key terms and considerations to help maximize this opportunity.

Luke Corry is a Supervisor, Resource Allocation, with the Illinois State Board of Education. Resources associated with this article can be reached via iasb.com/Journal.